Medicalgorithmics (MDG.WA)

Everything can change in a heartbeat.

Rating: BUY | Price Target: PLN 45 | Current Price: PLN 28 | Upside: +61%

Old Harbor Research · March 30, 2026

For informational purposes only. Not investment advice. The author may hold a personal position in MDG.WA. All data sourced from publicly available filings. This piece is a summary. Please read the full report.

Medicalgorithmics S.A. (MDG.WA) is a Warsaw-listed AI cardiac diagnostics company that has undergone a fundamental business model transformation since 2022. The market is pricing MDG as an unproven micro-cap with uncertain profitability and an unusual governance situation. Our differentiated view is that this is a structurally transformed business, the revenue inflection the market has been waiting for has finally arrived, and the active key shareholder is incentivized and positioned to maximize share price appreciation over at least the next twelve months. We initiate with a BUY rating and a 12-month base case price target of PLN 45.

What the Company Is Today

After divesting its ECG hardware distributor (Medi-Lynx) in 2022, MDG entered a strategic investment agreement with Biofund Capital Management that moved the business toward higher-value B2B AI software partnerships. The transaction brought in Kardiolytics Inc. and its two AI platforms—DeepRhythmAI (DRAI), a set of deep learning algorithms for ECG heart rhythm analysis, and VCAST, a CT-based coronary analysis platform. MDG contributed the critical input Kardiolytics needed: a proprietary annotated ECG dataset covering more than 3.6 million days of recordings (250+ billion heartbeats) accumulated through its PocketECG devices over the prior decade.

The result is a fundamentally different company from its hardware-focused predecessor: a capital-light AI software business with diversified distribution, cutting-edge algorithms, and a complementary optionality asset in a market that has already produced a multi-billion-dollar comparable.

MDG still offers hardware, including a new line of patch devices which come with the company’s software natively, but “services” now represent 94% of MDG’s revenue (as of 9M 2025). The per-session economics improve with scale and require no incremental hardware capital.

The Revenue Inflection

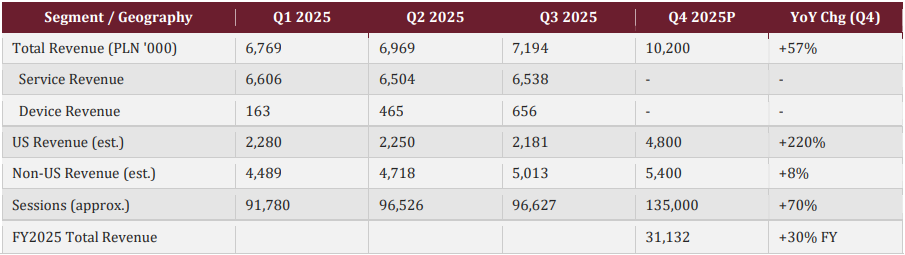

Revenue for the first nine months of 2025 reached PLN 20.9M (+20% YoY). The Q4 2025 preliminary result of PLN 10.2M (+57% YoY, +42% QoQ) brings the FY2025 total to approximately PLN 31.1M (+30% YoY). The rate of acceleration, from +20% on a nine-month basis to +57% in Q4 alone, confirms that the inflection is driven by the commercial conversion of 2025 partner agreements and the anchor US independent diagnostic testing facility (IDTF) integration.

The anchor IDTF exceeded USD 300k/month in November and USD 400–450k in December alone. DRAI processed 420,000+ sessions in FY2025 (+56% YoY). Q4 2025 marked the company’s first EBITDA-positive quarter (PLN +1.0M on PLN 10.2M revenue). The Q4 2025 EBITDA inflection is evidence that this model works at scale.

Costs are scaling sub-linearly with revenues as operating leverage emerges. In the first nine months of 2025, adjusted operating costs grew 6% YoY against 20% revenue growth, a 14-percentage-point spread that provides clear evidence of the operating leverage thesis materializing.

The Investment Case

MDG operates across two related AI cardiac diagnostics verticals. We frame the investment around two primary (1 and 2) and two secondary (3 and 4) pillars.

Pillar 1: The ECG/DRAI business is a standalone buy.

The DRAI competitive moat is defensible because the the training dataset cannot be replicated without years of data collection and annotation. MDG’s dataset of over 3.6 million days of ECG recordings represents a decade of accumulation. Clinical validation is provided by the MARTINI Study, the world’s largest published AI study in cardiac arrhythmia diagnosis, involving over 14,000 patients and more than 200,000 days of ECG data. DRAI demonstrated 14 times fewer missed diagnoses than trained ECG technicians. The study was published in Nature Medicine in February 2025 and led directly to multiple contract signings, including a competitive displacement: in November 2025, the largest private IDTF in the United Kingdom, which had been using a competing ECG analysis product, chose to switch to DRAI following the publication.

DRAI has FDA 510(k) clearance (updated Q2 2025), CE certification, Health Canada approval, and TGA approval in Australia. Twenty new commercial agreements were signed in 2025, adding partners across the US, Canada, Australia, the UK, and continental Europe. Agreements typically carry minimum volume commitments and multi-year terms, and the intensive integration processes make switching to competing platforms expensive and administratively taxing.

Management’s own ESOP, introduced in November 2025, uses annual revenue targets of PLN 55M (2025), PLN 60M (2026), and PLN 75M (2027) as vesting conditions, implying management’s expectations exceed our FY2026 base case estimate of PLN 58M. The ECG business’s revenue visibility is very good, with a roughly PLN 40M run rate as of the latest reporting and more partners going through the integration process.

Pillar 2: VCAST is an undervalued option on a multi-billion-dollar market.

VCAST is a software platform that uses AI algorithms to segment coronary vessel anatomy from cardiac CT scans and compute a simulated fractional flow reserve (CT-FFR) score, a non-invasive alternative to cardiac catheterization. The system creates an interactive 3D model of the heart, simulates fluid dynamics, performs risk analyses, and simulates the personalized effects of potential procedures.

VCAST obtained CE certification in October 2024 and has signed three distribution agreements (Turkey, Scandinavia, Saudi Arabia). An FDA 510(k) submission is in preparation, with management targeting clearance in H2 2027.

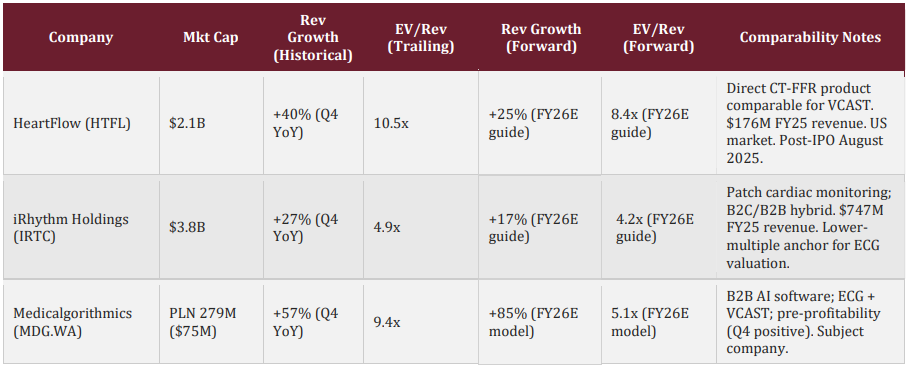

The most directly comparable public company is HeartFlow (HTFL), which IPO’d on the NYSE in August 2025 and trades at a $2.1B market capitalization on $176M FY2025 revenue with approximately 30% market share.

A key architectural distinction: VCAST is designed as a fully cloud-native autonomous system that processes CT-FFR analyses without requiring a human technician in the analysis loop. This is unlike HeartFlow’s workflow, which requires technician review before results reach the doctor. The practical consequences are faster turnaround times, lower cost per analysis, and a gross margin profile not encumbered by labor costs.

We assign zero near-term revenue value to VCAST in our base case to properly frame the investment; the core ECG business is sufficient justification for a BUY rating without any speculative VCAST contribution.

Pillar 3: SCAPIS participation could reframe the addressable market.

VCAST is being used to process cardiac CT data for SCAPIS, a landmark longitudinal cardiovascular imaging study at Lund University involving 30,000+ subjects. Prior SCAPIS data found that 42.1% of adults aged 50–64 without known coronary artery disease had measurable atherosclerotic burden. If VCAST is validated as a screening modality in this setting, the addressable market expands beyond the diagnostic CT-FFR market that HeartFlow addresses. SCAPIS simultaneously serves as a large-scale training dataset, in theory enhancing VCAST’s algorithmic efficacy.

Pillar 4: A US exchange listing would eliminate the structural discount.

MDG generates most of its revenue in US dollars from US customers, and its closest comparables trade in New York. Warsaw’s average daily dollar volume of approximately $2M structurally excludes most institutional capital. Management has explicitly stated that preparations for a 2026 entry into US capital markets are underway. A dual listing or ADR on the Nasdaq would expand the investor base and facilitate price discovery against comparables without requiring any further business development.

Valuation

Our primary methodology is EV/Revenue applied to FY2026E estimates, consistent with pre-profitability AI medtech peers. Revenue estimates are derived from a bottom-up analysis based on publicly disclosed partner run rates and contractual minimums.

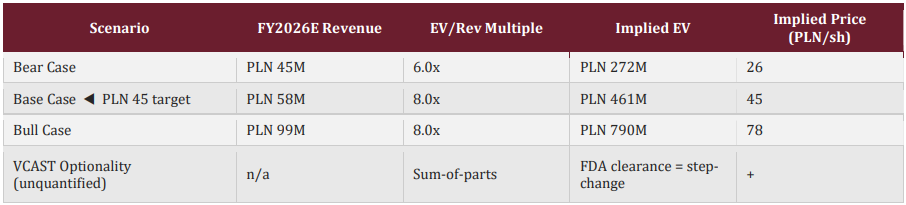

The base case return is driven by revenue growth, not multiple re-rating. At the PLN 45 price target, MDG would trade at 8.0x FY2026 revenue on a trailing basis, a compression from today’s 9.4x trailing. The thesis does not require the market to become more generous with its valuation, only that contracted partners convert at rates consistent with expectations.

At the current share price of PLN 28.00, MDG is trading at approximately 5.1x our FY2026E revenue estimate, a modest premium to iRhythm at 4.2x forward, despite MDG growing at +85% forward versus iRhythm’s +17%, operating a pure B2B AI software model with near-zero marginal cost per additional session, and carrying an optionality asset in VCAST that iRhythm does not.

Governance

Biofund Capital Management holds 13.8% of MDG’s equity following two secondary sales in September 2025 and January 2026, which reduced its stake from approximately 50% at the time of initial investment. Biofund simultaneously provides the primary debt facility, facilitates client relationships, and has one co-founder (Dr. Kris Siemionow) serving as President of MDG’s Management Board.

The two secondary sales were explicitly described by the company as preparations for entry into the US capital markets. The January 2026 transaction attracted Nationale-Nederlanden PTE as an 8.3% shareholder, the largest institutional equity investor in Central Eastern Europe. Biofund has committed to a 12-month lock-up on its remaining shares. In January 2026, Biofund also voluntarily waived its 3% revenue commission and eased loan terms for the company on the existing debt facility.

As a VC firm, Biofund intends to exit its remaining stake at some point following the lock-up. This creates a need for President succession as Dr. Siemionow departs, and no succession plan has been announced as of the date of this report, representing a key risk in the company’s future.

Key Risks

Partner integration delays are the near-term bear case. If integrations convert six months later than expected or fail to ramp sessions along expected timelines, FY2026 revenue could fall to PLN 48–52M. A 12-month delay would push revenue toward the PLN 45M bear case. This is a timeline risk, not a technology or market risk.

Customer concentration is a structural concern. The anchor US IDTF represents most of MDG’s revenues in recent months following its integration ramp. One or multiple key clients could be acquired by larger entities that transition to preferred technologies rather than renewing contracts.

A full Biofund exit creates significant governance and succession risk upon the departure of Dr. Kris Siemionow as President of the Management Board if a proper succession plan with a qualified executive replacement is not organized ahead of time. This is not an immediate risk, as shares are locked up into 2027.

Additional risks include VCAST FDA regulatory risk, FX exposure (US dollar revenues against a Polish zloty cost base without hedging), a thin cash buffer (PLN 3.0M as of 30 September 2025), competitive response from larger players, US healthcare policy and reimbursement changes, and intangible asset impairment risk (PLN 84.4M intangibles represent 80% of total assets).

Near-Term Earnings Expectations

In a March 16, 2026 interview, Dr. Siemionow indicated he expects positive EBITDA throughout 2026 and saw 50%+ YoY growth in February. He expects two or three contract signings per quarter, with a Q2 signing currently expected to be one of the largest European players in the market. He added that a recent DRAI update added language support beyond English, implying the opening of markets including France and Germany. He expects significant revenues from VCAST in H2 2026 and FDA clearance in H2 2027.

The FY2025 Annual Report is expected on April 28, 2026.

This piece summarizes Old Harbor Research’s full report on Medicalgorithmics S.A. (MDG.WA), published March 29, 2026. The full report includes a partner-by-partner revenue breakdown, detailed financial analysis, and expanded risk discussion. Read the full report.

For informational purposes only. Not investment advice. The author may hold a personal position in MDG.WA. All financial data sourced from publicly available filings (Q3 2025 Interim Report; Q4 2025 Preliminary Press Release dated 7 January 2026). Currency conversions assume USD 1 = PLN 3.72, verified March 29, 2026.

If you found this report to be worth your time, please consider sharing it. Thank you!